Are U.S. Markets Bubbling Up?

With new all-time highs this week in the S&P500 and the Dow Jones Industrial Average (DJIA), many are starting to worry about potential bubbles, especially in equity markets. With the Federal Reserve purchasing $85 billion in assets each month, many fear that this year’s tremendous gains in the market are simply an inflated sense of growth, which will be quick to tumble back down.

Liz Ann Sonders, chief investment strategist at Charles Schwab, on the other hand strongly disagrees. In an article written for the Wall Street Journal, Sonders explains, “The bubblicious chatter needs to stop: Stocks are not in a bubble. Period.”

In a checklist of nine items that generally preclude the peak of a bull-market, only one item is currently in range: rising real interest rates. Some of the other out-of-range indicators include IPO activity and a shift toward defensive leadership. In addition, many endowments, foundations and pensions also remain under-exposed to equities, generally in favor of alternatives.

Standard & Poor’s and Strategas Research Partners reported the trailing price to earnings ratio (P/E) of the S&P500 as 17.6 compared with the average of 18.7, further providing support for a legitimate bull market, ruling out mispriced equities in terms of their earnings.

Although there seems to be significant talk of bubbles, Sonders did not however rule out a pullback in the market, especially with the likelihood that the Federal Reserve begins tapering off their bond-buying program, quantitative easing.

Is Long-Term Care Worth Caring About?

Between your personal auto policy, homeowners insurance, life insurance and health care plan, you probably feel quite covered as far as insurance is concerned. While all of those policies are beneficial and rather essential, we might be neglecting a large portion of insurable risk: long-term care. We so cautiously insure ourselves against perils during our working years, our driving years and our adult years, but what most fail to consider are their retired, elder years.

Like many, my grandparents never had long-term care insurance. Also like many, my grandparents lived into their 80’s. They paid out of pocket for skilled nursing for nearly a decade. In that time, hundreds of thousands of dollars were spent to ensure their comfort and safety. While long-term care becomes increasingly necessary, we may not need to take the brunt of the financial burden with our own hard-earned money.

This situation can be difficult to address because of emotional and financial concerns, but ensuring comfort and a decent quality of life are very important factors to consider. This common necessity of long-term care creates two potential options: self-insure or purchase long-term care insurance.

Self-insuring, or consciously electing to pay out of pocket for future long-term care needs, can be done in a couple of different fashions. If an individual has a large liquid net worth, they can pay out of pocket for care as if it was another monthly expense. The other self-insuring option is to spend down almost all of one’s assets and enroll in Medicaid. Depending on the circumstances, either might make sense. The other option is to purchase a long-term care policy, in which an individual pays a premium like any other insurance policy, and once qualifying for benefits, receives a fixed dollar amount per month (or day) to pay for long term-care.

One thing to consider when debating between self-insuring and enrolling in a long-term care policy is one’s estate. Although paying insurance premiums will decrease one’s current net worth, self-insuring has the potential to significantly decrease the value of one’s estate. So if leaving money for family or charities is important, you might want to seriously consider long-term care insurance.

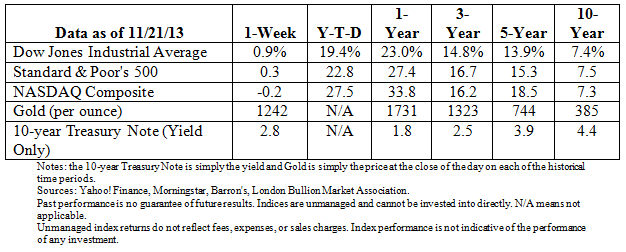

The Markets

This newsletter was prepared by Bourke Wealth Management.

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this e-mail with their e-mail address and we will ask for their permission to be added.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Gold represents the London afternoon gold price fix as reported by the London Bullion Market Association.

Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing.

Sources:

Barron’s (http://online.barrons.com/home-page)

Bloomberg (https://www.bloomberg.com/)

London Bullion Market Association (https://www.lbma.org.uk/)

Morningstar (http://www.morningstar.com/)

Horsesmouth (http://www.horsesmouth.com/ )

Wall Street Journal (http://online.wsj.com/home-page?mg=inert-wsj)

Yahoo! Finance (http://finance.yahoo.com/)