More Taper Talk

It feels like 2013 is all but behind us, and with each new statistical report we had word of the Federal Reserve tapering their $85 billion bond purchasing program, quantitative easing (QE). So here we are in the last few weeks of 2013, and once more the debate on fed tapering rages on.

To be clear, the decision to taper is not simply based on a few random statistics, rather it is a complex and dynamic decision.

That being said, the Fed’s list of reasons to end QE seems to grow a tad with each macroeconomic report. November’s rise in nonfarm payrolls was 203,000, making the August through November average 204,000 jobs per month. Comparing this to March through July’s average payroll of 156,000 per month evidences strengthening employment. In conjunction with this, the unemployment rate has dropped to 7.0%, approaching the Fed’s goal of 6.5%.

Finally, the Fed’s insistence on keeping the fed funds rate near zero even amidst a taper has seemingly calmed the markets.

To further support the move towards a taper, Congress appears to be ready to pass the new budget deal, taking a January 15th government showdown off the table.

Although the Fed’s outlook on growth remains modest to moderate, the evidence to support a quantitative easing taper continues to build.

What does a taper mean for you? Does it excite you to wean our economy off Federal Reserve purchases? Or does it make you nervous about your investments? Call us if you would like to hear our opinion on how this may affect you.

Congress’s New Deal

With October’s unfortunate fiscal meltdown fresh in their minds, members of Congress have drafted a new budget deal. According to Senator Patty Murray (D-WA) and Representative Paul Ryan (R-WI), the co-chairs of the bipartisan budget conference committee, Congress will approve the new budget deal. But what does this actually mean for America’s future of spending?

To the writers’ credit, the budget does resume planned spending cuts, bringing us closer towards a stable balance sheet. While maintaining Social Security and Medicare, in addition to not raising taxes, the budget is projected to achieve savings of $23 billion over the next 10 years.

Although the new budget does reduce government spending, one controversial sector remains primarily unchanged: defense spending. Under the new budget, U.S. defense spending in 2013 would come in at a whopping $520 billion. This would mean the United States spends $30 billion more on defense than all of the domestic programs under the discretionary budget combined.

Although the new budget perhaps does not accomplish everyone’s goals, it is an important step towards a functional and reliable government, moving past partisan issues. With governmental cooperation, US markets and even markets abroad could avoid fiscal uncertainty such as the 16 day Government shut down in October. And thanks to this budget, we shouldn’t have another shutdown come January 2014. So into the New Year we go, hopefully with no cliffs on the horizon.

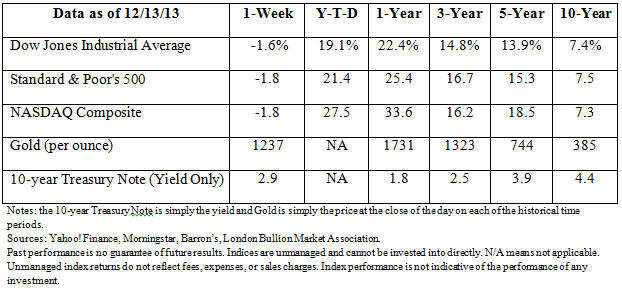

The Markets

This newsletter was prepared by Bourke Wealth Management.

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this e-mail with their e-mail address and we will ask for their permission to be added.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Gold represents the London afternoon gold price fix as reported by the London Bullion Market Association.

Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing.

Sources:

Barron’s (http://online.barrons.com/home-page)

Bloomberg (https://www.bloomberg.com/)

London Bullion Market Association (http://www.lbma.org.uk/pages/index.cfm)

Morningstar (http://www.morningstar.com/)

Horsesmouth (http://www.horsesmouth.com/ )

Wall Street Journal (http://online.wsj.com/home-page?mg=inert-wsj)

Yahoo! Finance (http://finance.yahoo.com/)